.jpg)

How Collateral Affects Small Business Lending: The Role of Lender Specialization

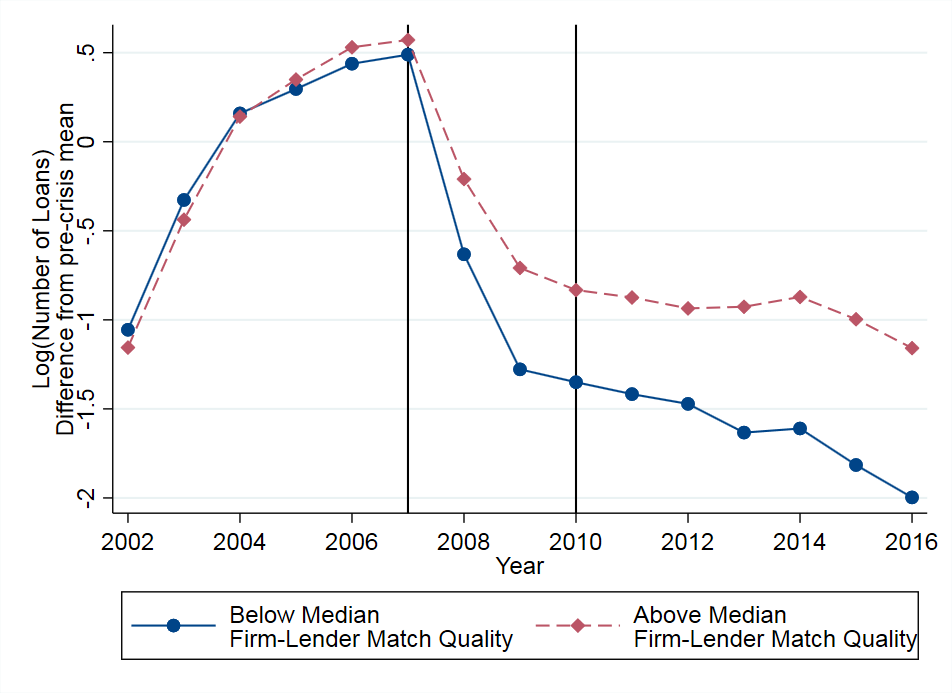

I study the role of collateral on small business credit access in the aftermath of the 2008 financial crisis. I construct a novel, loan-level dataset covering all collateralized small business lending in Texas from 2002-2016 and link it to the U.S. Census of Establishments. Using textual analysis, I quantify whether a lender is specialized in a borrower's collateral by comparing the collateral pledged by the borrower to the lender's collateral portfolio. I show that, post 2008, lenders reduced credit supply by focusing on borrowers that pledged collateral in which the lender specialized. This result holds when comparing lending to the same borrower from different lenders, and when comparing lending by the same lender to different borrowers. A 10% higher specialization in borrower collateral increases lending to the same firm by 1.2%. Abstracting from general equilibrium effects, if firms switched to lenders with the highest specialization in their collateral, aggregate lending would increase by 14.8%. Furthermore, firms borrowing from lenders with greater specialization in the borrower's collateral see a larger growth in employment after 2008. I identify the lender's informational advantage in the posted collateral to be the mechanism driving lender specialization. Finally, I show that firms with collateral more frequently accepted by lenders in the economy find it easier to switch lenders. In sum, my paper shows that borrowing from specialized lenders increases access to credit and employment during a financial crisis. Download Paper Here